In 2025, in-transit inventory stands as a major factor in shaping the financial impact on every business. Poor inventory management causes excess stock and slow turnover, which ties up capital and increases storage costs. This reduces business cash flow and profitability. Companies that mismanage inventory in transit face higher capital requirements. A closer look at recent industry data shows how these challenges develop:

Aspect | Impact on Business Financials |

|---|---|

Inventory Holding | 11.3% unit value rise plus longer holding periods raises capital use by 60% |

Inventory Investment | $10 million with extra holding can need $6.7 million more capital |

Financing Inventory in Transit | 60% advance rate means $2.7 million cash needed or higher accounts payable |

Inventory Turnover | Slow turnover strains working capital and lowers cash flow |

Consumer Behavior | Lower turnover leads to price cuts and higher risk of obsolescence |

Inventory to Sales Ratio | More inventory relative to sales increases capital needs |

Accurate tracking and financial reporting help reduce risk and prevent financial losses. Businesses that excel in financing inventory in transit, manage capital, and control risk, gain stronger financial health and efficiency. Focusing on financing inventory in transit, companies can unlock capital, improve financial outcomes, and reduce risk during transit.

Financial Impact of In-Transit Inventory

Cash Flow Effects

In-transit inventory directly influences a business’s cash flow. When goods move between locations, the company’s capital becomes tied up. This capital cannot be used for other business needs until the inventory arrives and becomes available for sale or production. Inventory often accounts for 25% to 30% of a company’s working capital. Delays in transit increase the time that capital remains locked, which can strain cash flow and limit flexibility.

Companies that track inventory location in real time can improve forecasting and manage cash flow more effectively. Aligning cash outflows with the arrival of inbound inventory helps optimize payment timing and reduces unnecessary capital hold. Shipment estimated times of arrival (ETAs) give treasury teams forward visibility, allowing them to adjust cash flow projections and payment terms if delays occur. Monitoring supplier financial status also enables early payments or supply chain finance, which helps manage working capital tied up in inventory. Integration between supply chain and treasury systems unlocks trapped liquidity, reducing dependency on short-term borrowing and lowering overall working capital requirements.

Tip: Reducing lead times by sharing sales data with suppliers and lowering minimum order quantities can free up working capital and improve cash flow.

Asset Valuation

Accurate asset valuation depends on proper recognition and tracking of in-transit inventory. The accounting treatment for goods in transit relies on shipping terms. Under FOB shipping point, the buyer records the inventory as soon as it ships. Under FOB destination, the seller keeps the inventory on their balance sheet until it arrives. Including or excluding in-transit inventory affects the inventory asset account and the accuracy of financial statements.

Fluctuations in in-transit inventory levels can cause discrepancies between recorded and actual inventory. These discrepancies may lead to errors in reported assets and cost of goods sold. Regular audits, real-time tracking, and clear inventory classification help maintain accurate asset valuation. Delayed receipt of in-transit inventory can understate inventory on the balance sheet, reducing the reported value of current assets. This reduction impacts liquidity ratios, such as the current ratio, making the business appear less liquid and potentially affecting loan eligibility or credit terms.

In-transit inventory consists of goods purchased but not yet received, and whether these are included in inventory depends on sale terms.

Proper accounting practices and technology help maintain accurate asset valuation and reduce risk.

Profitability

The financial impact of in-transit inventory extends to business profitability. Poor tracking and inaccurate reporting can distort cost of goods sold, leading to significant financial losses. For example, inventory distortion caused global losses of $818 billion in one year, with 56% due to stockouts and 44% from overstocks. Overbuying and misallocation, often caused by poor tracking, account for 53% of unplanned markdown costs in retail.

Impact on Profitability | Explanation | Quantitative Data / Example |

|---|---|---|

Stockouts caused by inaccurate inventory lead to missed revenue opportunities. | Retailers lose around $1.1 million per year due to stockouts. | |

Increased Holding Costs | Excess inventory ties up capital and increases carrying costs, reducing profitability. | Carrying costs can reach up to 41% of a product’s value. |

Inefficient Forecasting & Planning | Flawed data leads to poor demand forecasting, causing overstock or shortages. | 60% of manufacturers struggle with inaccurate inventory data. |

Operational Inefficiencies | Delays and errors in inventory data disrupt supply chain visibility and decision-making. | Overstocking contributes to billions in lost sales annually. |

Working Capital Misuse | Excess inventory ties up working capital that could be used elsewhere in the business. | Excess stock can cause up to 30% loss in annual profits. |

Inaccurate reporting of in-transit inventory causes discrepancies between recorded and actual stock levels. These discrepancies lead to lost sales from stockouts and increased holding costs from excess inventory. Inventory inaccuracies can cost businesses up to 10% of their annual revenue. Human errors, such as incorrect quantity entries, and supply chain disruptions, like partial shipments, often cause these issues. These inaccuracies ripple through operations, causing inefficiencies and reducing profits.

Note: Improving forecasting with real-time tracking and integrated communication optimizes inventory levels, minimizes excess capital lockup, and reduces risk to business profitability.

Understanding Goods in Transit

Definition

Goods in transit represent inventory that a business has purchased but not yet received. These items in transit have left the seller’s shipping dock and are moving toward the buyer’s location. According to international accounting guidelines, inventory recognition depends on when ownership transfers. Under FOB shipping point, the buyer owns the goods once they leave the seller. Under FOB destination, the seller keeps ownership until the goods arrive at the buyer’s facility. This distinction affects how a business records inventory on its balance sheet.

Goods in transit are counted as assets for the buyer once ownership transfers, even if the inventory has not physically arrived.

Inventory management teams must track these goods carefully to ensure accurate financial reporting.

Businesses must understand shipping terms to determine when to include goods in transit in their inventory records.

Note: Proper recognition of goods in transit ensures that a business values its inventory correctly and meets international accounting standards.

Why It Matters

Managing goods in transit plays a critical role in business success. Transportation connects suppliers, manufacturers, and customers, making it the backbone of inventory management. Efficient handling of goods in transit prevents stockouts and overstocking, which helps businesses avoid lost sales and excess storage costs. In 2025, advanced technologies like artificial intelligence, blockchain, and IoT give businesses real-time visibility into inventory and transit status. These tools help companies make better decisions, reduce risk, and improve fulfillment speed.

Businesses that track goods in transit closely can respond quickly to market changes. Real-time data from Transportation Management Systems and ERP platforms allow companies to adjust inventory levels and delivery schedules. This flexibility reduces transit times and storage needs, leading to higher customer satisfaction. As the demand for faster delivery grows, effective management of goods in transit becomes even more important for business competitiveness.

Timely and accurate tracking of inventory in transit supports better cash flow and asset valuation.

Businesses that excel at managing goods in transit gain a strong advantage in inventory management and fulfillment.

In-Transit Inventory on Financial Statements

Current Assets

Businesses must classify in-transit inventory as a current asset on their financial statements when they own the goods in transit. This classification depends on shipping terms. Under FOB shipping point, the buyer takes control and risk once the goods leave the seller. The buyer then includes the goods in transit as inventory on the balance sheet. Under FOB destination, the seller keeps ownership until delivery, so the seller lists the inventory as a current asset until the buyer receives it. Both IFRS and GAAP require businesses to value inventory, including goods in transit, at cost or net realizable value, whichever is lower. This approach ensures that the inventory value on financial statements reflects true business assets and supports accurate inventory valuation.

Goods in transit become part of the buyer’s inventory when control passes.

Inventory appears as a current asset on the balance sheet.

Businesses must disclose the method used for inventory valuation.

COGS Impact

The timing of recognizing goods in transit affects the cost of goods sold on financial statements. Ownership rules guide when a business includes these costs.

Under FOB shipping point, the buyer adds the cost of goods in transit to inventory immediately. This cost then moves to cost of goods sold when the business sells the inventory.

Under FOB destination, the buyer waits until delivery before recording the inventory and related costs.

Businesses must include all related costs—such as freight, insurance, and handling fees—in the total inventory cost.

Accurate accounting for goods in transit prevents errors in cost of goods sold and keeps financial statements reliable.

The timing of cost recognition helps businesses manage capital and maintain clear financial records.

Owner’s Equity

Goods in transit also influence owner’s equity on financial statements. When a business records inventory as a current asset, it increases total assets. This increase can improve the business’s financial position and owner’s equity. If a business fails to record goods in transit correctly, it may understate assets and owner’s equity. Accurate reporting of inventory and goods in transit ensures that financial statements show the true value of the business. This transparency supports better decision-making and builds trust with investors and lenders.

Note: Proper tracking and reporting of goods in transit help businesses maintain strong financial health and accurate financial statements.

Accounting Rules for Goods in Transit

Recognition Timing

Recognition timing for goods in transit plays a critical role in business financial statements. The timing depends on when control and ownership transfer from seller to buyer. In some cases, sellers ship goods under terms that appear to transfer control at shipment, but they retain certain risks or replacement obligations. This situation, sometimes called "synthetic FOB destination," means the seller must carefully assess if control has truly passed. The seller evaluates if the buyer has received the significant risks and rewards of ownership. This decision affects when the business recognizes revenue and includes goods in transit in inventory accounting.

Key timing considerations include:

Reviewing shipping terms and risk retention.

Assessing customer acceptance and contractual obligations.

Determining if control transfer aligns with ASC 606 standards.

The timing of recognition impacts both revenue and accounting for inventory. Businesses must use judgment to ensure accurate reporting of goods in transit.

FOB Shipping Point vs. Destination

Shipping terms directly influence how a business records goods in transit. The two most common terms are FOB shipping point and FOB destination. The following table summarizes the main differences:

Aspect | FOB Shipping Point | FOB Destination |

|---|---|---|

Ownership Transfer | Ownership and risk transfer to buyer when goods are shipped | Seller retains ownership and risk until goods are delivered |

Inventory Recognition | Buyer records inventory at shipment point | Buyer records inventory upon receipt at destination |

Revenue Recognition | Seller recognizes revenue when goods leave seller's facility | Seller recognizes revenue upon delivery to buyer |

Transportation Costs | Buyer bears transportation costs from shipping point | Seller bears transportation costs until delivery |

For example, if a business orders goods under FOB shipping point, it assumes ownership and risk as soon as the goods leave the seller’s facility. The business must include these goods in transit in its inventory accounting and financial statements. Under FOB destination, the seller keeps ownership and responsibility until delivery. The business only records the goods in transit as inventory after receiving them.

Reporting Best Practices

Accurate reporting of goods in transit supports compliance and strong business performance. Businesses should follow these best practices for accounting for inventory and inventory accounting:

Regularly track inventory movements to detect loss and maintain balanced stock levels.

Conduct cycle counts when receiving new goods in transit to verify arrivals and resolve discrepancies.

Automate inventory management with software for real-time updates and reduced human error.

Keep organized stockrooms to minimize loss or misplacement of goods in transit.

Clearly define reporting requirements, including SKU-level details, descriptions, pricing, and remaining stock.

Tip: Businesses should audit goods in transit by verifying bills of lading against shipping manifests and receipts. This process ensures accurate location tracking and supports audit trails.

Businesses must also coordinate with third-party warehouses, maintain thorough documentation, and use technology such as barcode scanners or RFID. Reconciling physical counts with perpetual records and complying with standards like GAAP or IFRS strengthens internal controls. These steps help businesses achieve accurate, timely, and compliant reporting for goods in transit.

Risk Management for In-Transit Inventory

Common Risks

Every business faces significant risk when managing inventory in transit. Over 60% of supply chain theft incidents happen during transit, making theft a leading cause of loss. The most common risks include:

Pilferage, full load theft, and fraudulent pickups

Tampering, insider collusion, and route deviation

Hijacking and cyber-fraud targeting shipment data

Shipment damage from poor handling or packaging

Delays caused by lack of real-time visibility or poor carrier vetting

About 37% of companies struggle to track shipments during the mid-mile phase, which increases the risk of inventory loss. Many businesses only discover shipment damage after delivery, leading to rejected shipments and lost customer trust. Repeated disruptions can halt production, delay orders, and damage brand reputation. Prevention strategies such as physical security, thorough carrier vetting, and real-time GPS tracking help reduce the risk of loss during transit.

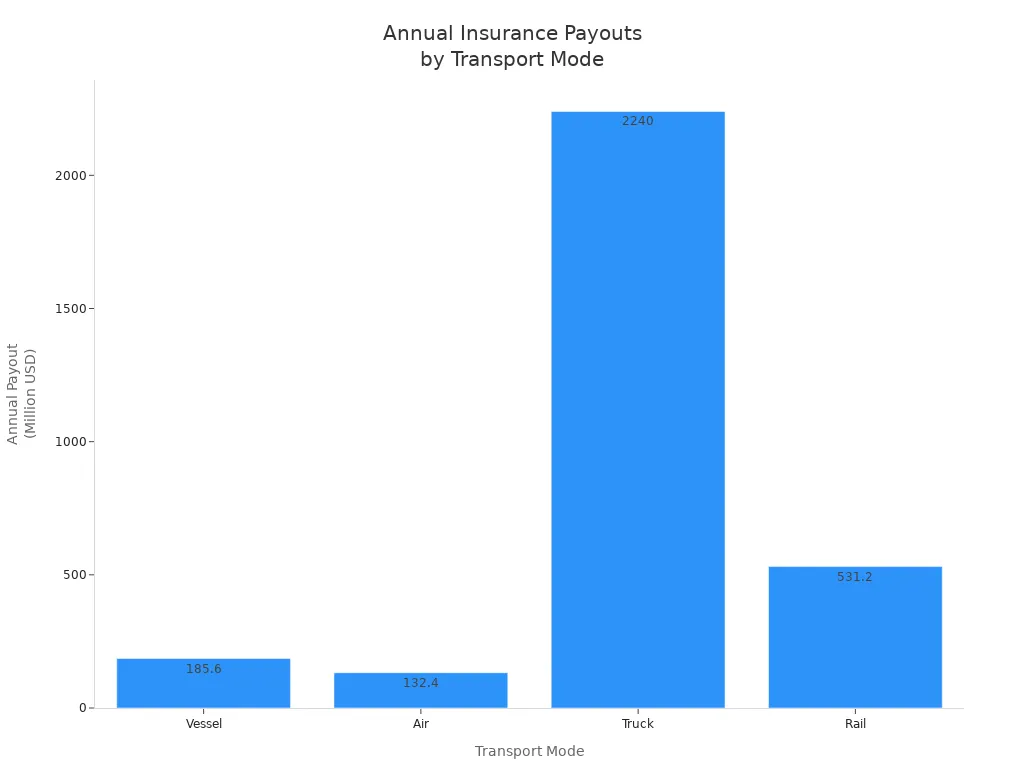

Insurance Coverage

Insurance plays a vital role in protecting business assets during transit. Most businesses use freight or cargo insurance to cover loss or damage. Coverage options include replacement cost and net selling price valuations. Proper packing and labeling reduce the risk of damage, while high-value shipments may need extra liability coverage. The average claim rate for in-transit inventory is 0.32%, with an average claim payment of $2,568. Annual payouts in the U.S. freight industry exceed $3 billion.

Aspect | Details |

|---|---|

Insurance Type | Freight or cargo insurance policies covering loss or damage during transportation |

Coverage Options | Replacement cost and net selling price valuations |

Additional Protection | Proper packing, labeling, and sometimes separate liability coverage from third-party insurers |

Average Claim Rate | 0.32% of shipments |

Average Claim Payment | $2,568 per claim |

Estimated Annual Payout | Over $3 billion in the U.S. freight industry |

Up to 11% of unit loads arrive damaged, costing businesses about 0.5% of gross sales each year. Insurance helps offset direct and indirect costs, but proactive prevention remains essential.

Internal Controls

Strong internal controls protect business inventory in transit and reduce the risk of loss. Effective controls include:

Tracking systems and regular reconciliation of material movement

Access controls and inventory movement logs to prevent unauthorized access

Physical verification and management approval for inventory adjustments

Control Area | Risks Addressed | Key Controls Implemented |

|---|---|---|

Tracking and Reconciliation of Material Movement | Miscommunication, discrepancies, loss, theft during transit | Use of tracking systems; regular reconciliation; secure transportation; verify receipt at each location |

Access Control and Inventory Movement Logs | Unauthorized access, theft, inadequate tracking, fraud risk | Implement access controls; maintain logs; enforce segregation of duties |

Physical Verification and Authorization | Discrepancies, unauthorized adjustments, errors or fraud | Conduct regular counts; investigate variances; require management approval for adjustments |

Businesses that invest in real-time tracking, thorough documentation, and regular audits can minimize the risk of inventory loss. These steps ensure that inventory in transit remains secure and accurately reported.

Financing Inventory in Transit

Using Inventory as Collateral

Many businesses use financing inventory in transit as a way to unlock capital and support daily operations. Once goods ship and ownership transfers, companies can count these items as inventory. This status allows them to pledge in-transit inventory as collateral for short-term loans or credit lines. Lenders often base the loan amount on a percentage of the inventory’s resale value. If a business defaults, the lender can claim the inventory to recover the loan. Proper documentation and clear ownership records remain essential for this process. By leveraging in-transit inventory, businesses gain flexibility, improve working capital, and strengthen supplier relationships. This approach also provides a competitive edge by enabling continuous cash flow and supporting growth.

Businesses secure financing against inventory in transit, increasing funding options.

This method improves liquidity and supports financial stability.

Purchase order financing helps companies fulfill large orders and maintain capital flow.

Supply Chain Financing

Supply chain financing offers another solution for businesses managing inventory in transit. This method involves third-party lenders or financial institutions providing funds based on the value of goods moving through the supply chain. Financing inventory in transit through supply chain programs helps companies pay suppliers faster, negotiate better terms, and reduce risk. These programs often use technology to track inventory and confirm shipment status, which lowers financial risk and increases transparency. Supply chain financing supports financial stability by ensuring businesses have enough capital to meet demand and manage unexpected disruptions.

Benefit | Description |

|---|---|

Faster Supplier Payments | Improves supplier trust and reliability |

Enhanced Negotiation Leverage | Allows better pricing and contract terms |

Reduced Risk | Minimizes disruptions and supports cash flow |

Improved Working Capital | Frees up capital for other business needs |

Cash Flow Solutions

Effective cash flow solutions help businesses manage the financial impact of inventory in transit. Real-time tracking with GPS, RFID, and logistics software gives companies visibility into their inventory. This visibility reduces delays, lowers holding costs, and prevents excess capital from being tied up. Working with logistics providers and using just-in-time delivery models further improves inventory efficiency. Technology platforms that offer transportation visibility and supply chain management tools help businesses optimize inventory timing and reduce risk. These solutions support better financial outcomes and ensure that capital remains available for growth and operations.

Tip: Companies that invest in advanced tracking tools and partner with reliable logistics providers can reduce risk, improve cash flow, and maintain strong financial health.

Best Practices for 2025

Tracking Tools

Businesses in 2025 rely on advanced tracking tools to improve inventory management and fulfillment. IoT-driven shipment monitoring systems now offer real-time updates on environmental conditions, predictive maintenance, and detailed handling insights. These features help maintain the quality of sensitive shipments, such as pharmaceuticals and perishables. Integration with blockchain technology increases security and traceability, giving businesses better inventory visibility across the supply chain. Wiliot, recognized by Gartner, delivers platforms that monitor inventory health, detect errors, and track freshness. Companies using these solutions have seen a 90% drop in temperature-related shrinkage and a 70% reduction in mis-shipments. These results show how real-time tracking tools support business fulfillment and reduce risk.

Financial Planning

Effective financial planning depends on accurate inventory management and real-time visibility. Businesses that use advanced tracking technology can lower expedite rates by up to 90% and reduce inventory levels by 40%. This improvement leads to higher profitability and better fulfillment. Planner efficiency rises as much as 300%, with fewer errors and less manual work. Integration with MRP and ERP systems supports scalable growth and aligns inventory with actual demand. Real-time monitoring helps businesses spot shipment delays, theft, or damage early, which prevents larger financial losses. Accurate arrival data allows for better warehouse preparation and resource allocation. Data-driven decisions from tracking tools give businesses a competitive edge in financial planning and fulfillment.

Reducing Financial Risk

Businesses must address risk at every stage of inventory management. Selecting reputable carriers and using specialty services for fragile or high-value goods reduces loss risk. Maintaining detailed shipment inventories with unique identifiers helps recover losses. Immediate inspection of goods upon receipt prevents insurance issues. Clear agreements on financial responsibility, along with insurance programs, transfer risk and protect assets. Protective packaging and fewer transit stops lower the chance of damage. Careful selection of personnel ensures proper handling. Robust contingency plans, alternative suppliers, and communication protocols prepare businesses for disruptions. Regular reviews and simulations keep risk management strategies effective. These steps help businesses minimize financial risk and maintain strong fulfillment performance.

In 2025, business leaders must prioritize the financial impact of in-transit inventory. Accurate tracking reduces holding costs by up to 30% and improves order accuracy, directly supporting financial stability. Financing inventory in transit unlocks working capital, giving business teams more flexibility. Real-time tracking and risk management frameworks help business owners reduce financial losses and improve planning. Companies should review their financial processes, adopt new technologies, and consult experts to optimize financing inventory in transit. By integrating advanced tools, business teams can transform inventory into a strategic financial asset and strengthen business resilience.

Key steps for 2025:

Implement real-time tracking for in-transit inventory.

Integrate financing inventory in transit with business planning.

Monitor financial KPIs and review business processes regularly.

FAQ

What is inventory in transit?

Inventory in transit refers to goods that a company has purchased but not yet received. These items move between locations after leaving the seller but before arriving at the buyer’s facility. Companies must track these goods for accurate financial reporting.

How does in-transit inventory affect cash flow?

In-transit inventory ties up company capital. The business cannot use this money for other needs until the goods arrive. Delays in transit can increase the time capital remains locked, which may strain cash flow.

Who owns goods in transit?

Ownership depends on shipping terms. Under FOB shipping point, the buyer owns the goods once they leave the seller. Under FOB destination, the seller keeps ownership until the goods reach the buyer’s location.

What risks are common with inventory in transit?

Theft, damage, and shipment delays are common risks. Companies also face loss from poor tracking or miscommunication. Insurance and real-time tracking tools help reduce these risks and protect business assets.

See Also

How Incorrect Shipments Significantly Affect Your Financial Results

New EDI Tracking Technologies Enhancing Future Shipment Transparency

Maximizing Productivity Using Pick To Cart Solutions In 2025

Three Methods Lean Logistics Improves Sustainable Supply Chains

Lean Logistics Enables Quick And Eco-Friendly Supply Chain Success